Model Assessment

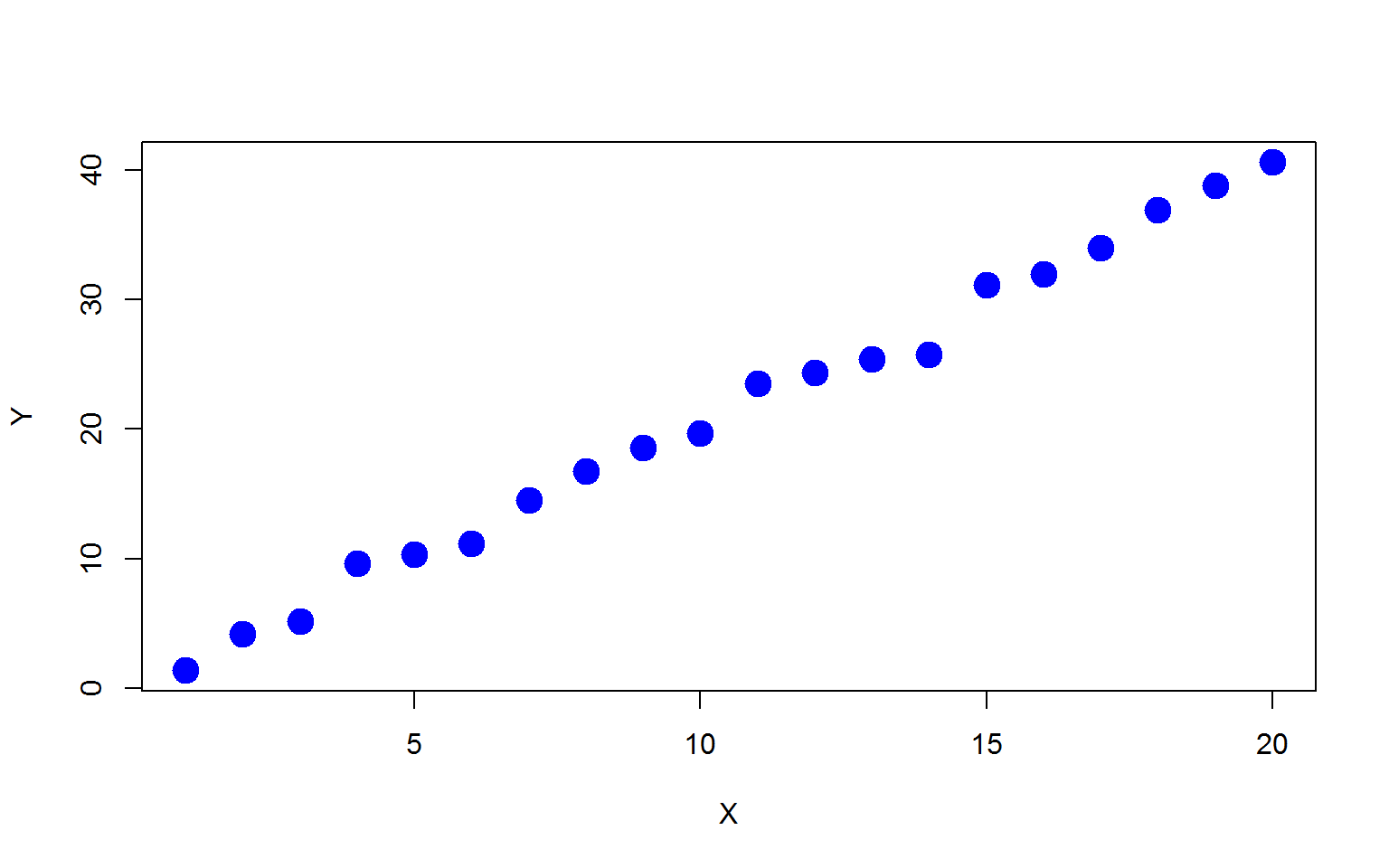

First, let’s generate a simple simulation example with \(x=1,2,\cdots,20\) and \(y\) is a linear function of \(x\) with some additive random noise:

\[ y_i=2x_i+\epsilon_i, \quad \epsilon \sim N(0,1). \]

n=20

x=1:n

set.seed(1)

e=rnorm(n,mean=0,sd=1)

y=x*2+e

plot(x,y,xlab="X",ylab="Y",pch=19,col="blue",cex=2)

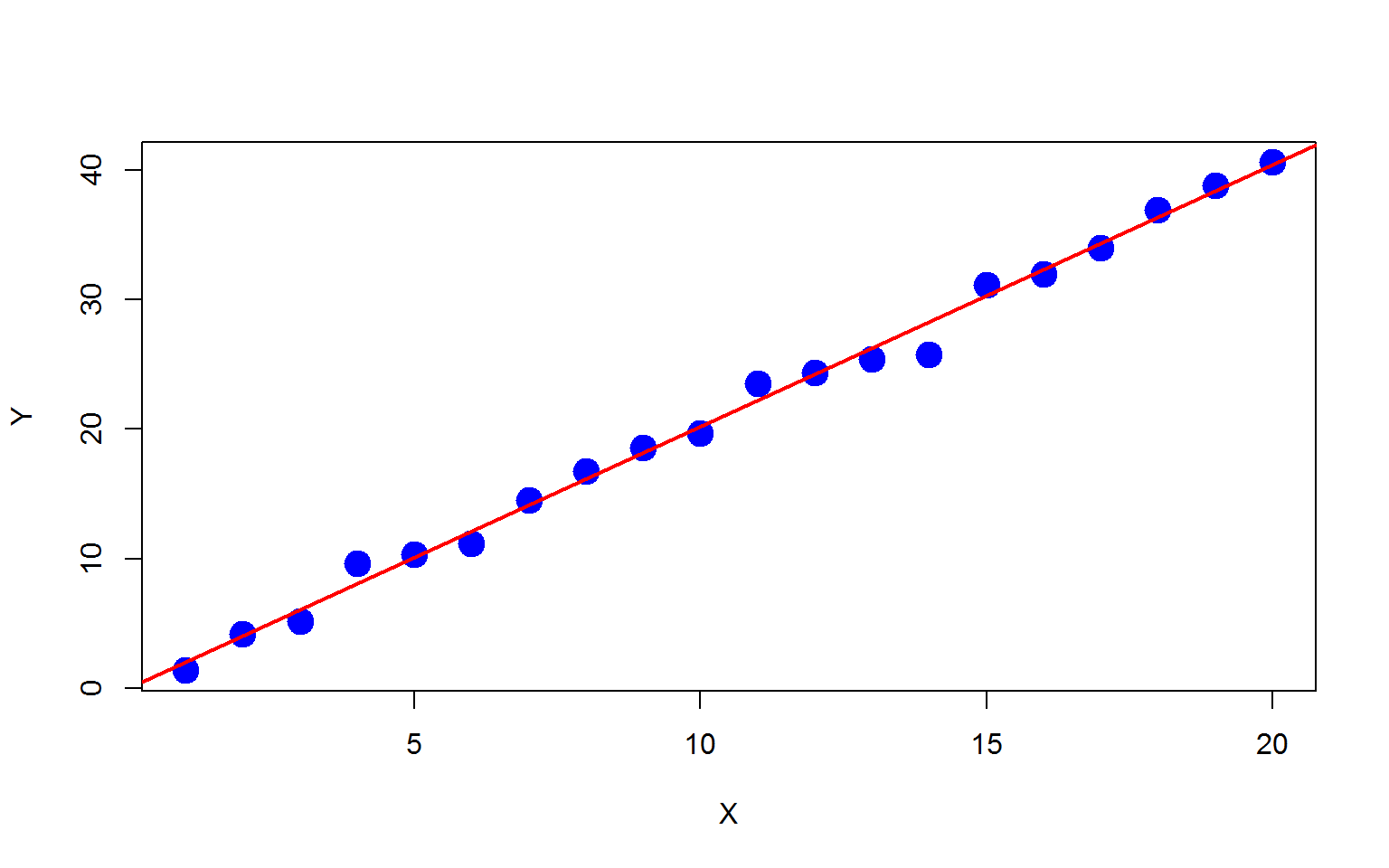

Then we fit a simple linear regression on the dataset.

f=lm(y~x)

plot(x,y,xlab="X",ylab="Y",pch=19,col="blue",cex=2)

abline(f,col="red",lwd=2)

f$fit

## 1 2 3 4 5 6 7

## 1.985490 4.007072 6.028655 8.050237 10.071820 12.093402 14.114985

## 8 9 10 11 12 13 14

## 16.136568 18.158150 20.179733 22.201315 24.222898 26.244480 28.266063

## 15 16 17 18 19 20

## 30.287645 32.309228 34.330810 36.352393 38.373976 40.395558

f$residual

## 1 2 3 4 5 6

## -0.6119435 0.1765711 -0.8642834 1.5450435 0.2576879 -0.9138708

## 7 8 9 10 11 12

## 0.3724441 0.6017572 0.4176313 -0.4851210 1.3104660 0.1669455

## 13 14 15 16 17 18

## -0.8657208 -2.4807627 0.8372856 -0.3541615 -0.3470007 0.5914432

## 19 20

## 0.4472457 0.1983433

mean(f$residual^2) #MSE on training set

## [1] 0.7768427

In-sample Optimism

The MSE on the training set is obviously smaller than the true value (since this is a simulation example, we do know the MSE.

set.seed(2)

e2=rnorm(n,mean=0,sd=1)

y2=x*2+e2

mean((y2-f$fit)^2) #MSE on new responses

## [1] 1.061651

You can see that the MSE on the training set is too optimistic. Now let’s find out the expected loss on the training samples for new response values \[ \frac{1}{n}\sum_{i=1}^n E_{Y^0}\left [ L(Y_i^0, \hat{f}(x_i))|\mathcal{T}\right ]. \]

iter=1000

mse=rep(0,iter)

for (i in 1:iter){

set.seed(i+1)

e3=rnorm(n,mean=0,sd=1)

y3=x*2+e3

mse[i]=mean((y3-f$fit)^2)

}

mean(mse) #Estimate of the expected loss on training set with new Ys

## [1] 1.043732

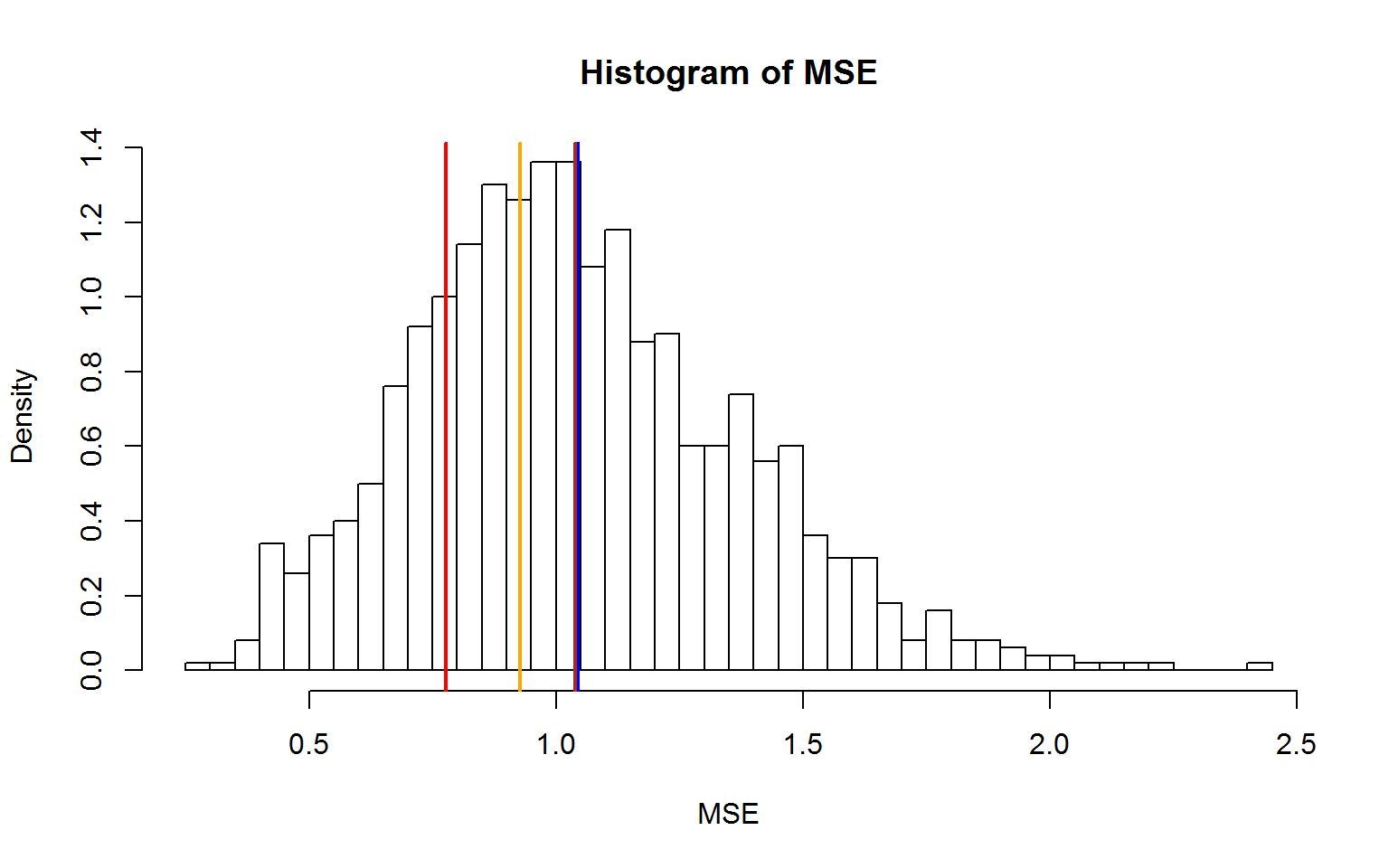

hist(mse,nclass=50,xlab="MSE",ylab="Density",freq=F,main="Histogram of MSE")

abline(v=mean(f$residual^2),col="red",lwd=2)

abline(v=mean(mse),col="blue",lwd=2)

In-sample optimism is defined as the difference between the expected loss on the training

samples for new response values and the training error

In-sample optimism is defined as the difference between the expected loss on the training

samples for new response values and the training error

\[

op=\frac{1}{n}\sum_{i=1}^n E_{Y^0}\left [ L(Y_i^0, \hat{f}(x_i))|\mathcal{T}\right

] - \overline{err}.

\]

If we can find out the in-sample optimism, we can have a better estimate of the expected loss on the training samples for new response values.

\[

\frac{1}{n}\sum_{i=1}^n E_{Y^0}\left [ L(Y_i^0, \hat{f}(x_i))|\mathcal{T}\right ]=op+\overline{err}.

\]

#In-sample optimism

op=mean(mse)-mean(f$residual^2)

op

## [1] 0.2668894'

#A better estimate of performance on test x values

op+mean(f$residual^2)

## [1] 1.043732

Mallow Cp and AIC are developed based on the above idea with the fact that

\[

E_y(op)=\frac{2}{n} \sum_{i=1}^n Cov(\hat{y},y_i).

\]

K-fold Cross-validation

We can estimate the generalization performance through cross-validation. For linear models, we can easily calculate the leave-one-out CV without fitting models n times.

\[

\frac{1}{n}\sum_{i=1}^n [y_i-\hat{f}^{-i}(x_i)]^2 = \frac{1}{n}\sum_{i=1}^n \left[

\frac{y_i-\hat{f}(x_i)}{1-H_{ii}}\right ]^2, \quad where \quad \hat{f}=Hy.

\]

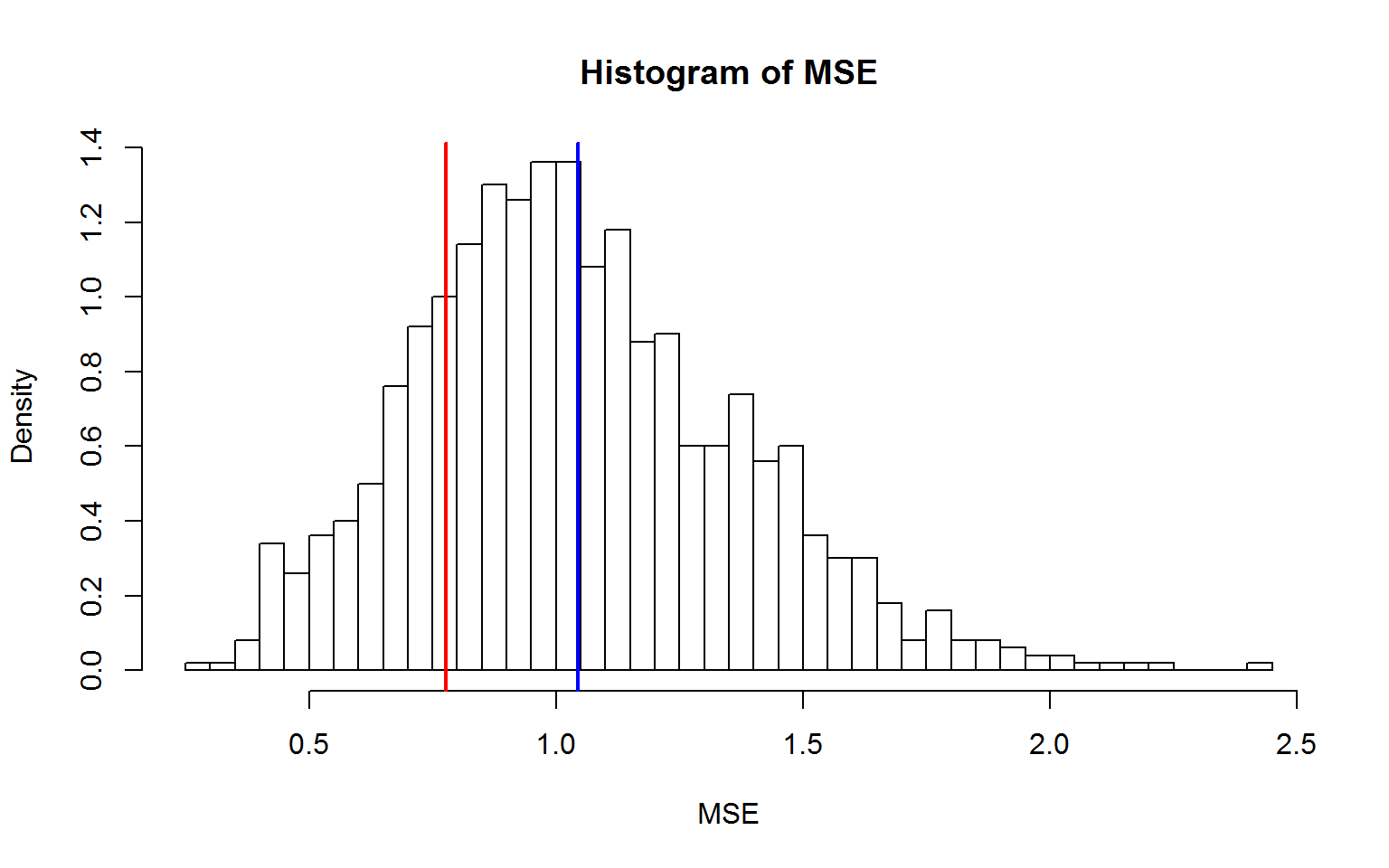

#Hat-diagonal values (leverage)

hat.diag=influence(f)$hat

#LOOCV: PRESS (predicted residual error sum of squares)

press=mean(((y-f$fit)/(1-hat.diag))^2)

press

## [1] 0.927807

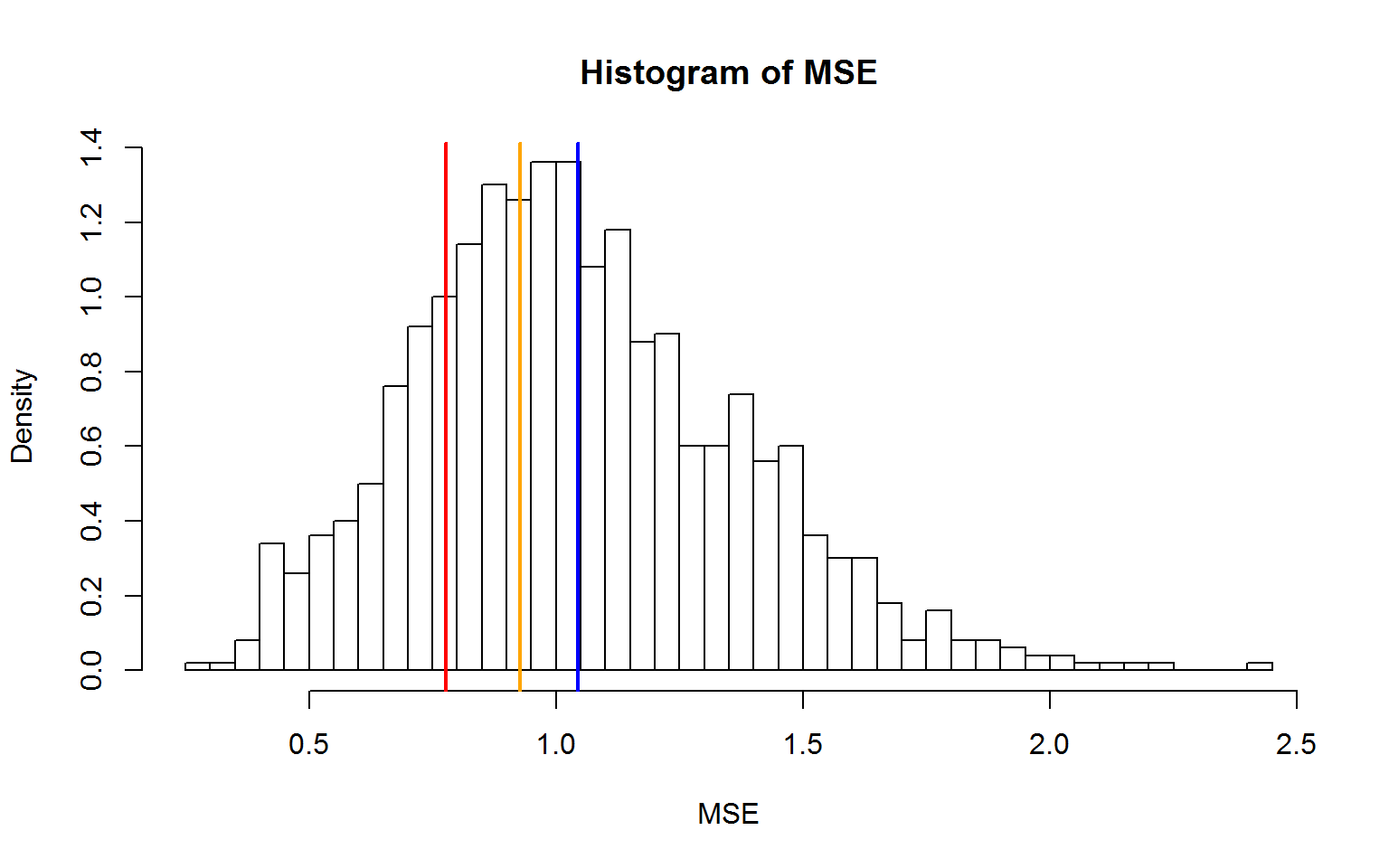

hist(mse,nclass=50,xlab="MSE",ylab="Density",freq=F,main="Histogram of MSE")

abline(v=mean(f$residual^2),col="red",lwd=2)

abline(v=mean(mse),col="blue",lwd=2)

abline(v=press,col="orange",lwd=2)

Out-of-bag (OOB) Samples in Bootstrapping

we can also use out-of-bag (OOB) samples in bootstrapping to estimate the generalization performance of a model. Let’s first see what the OOB samples are.

#Use Out-of-bag (OOB) estimate to evaluate performance

set.seed(1)

boot.id=sample(1:20,size=20,replace=T)

boot.id

## [1] 6 8 12 19 5 18 19 14 13 2 5 4 14 8 16 10 15 20 8 16

setdiff(1:20,boot.id) #out-of-bag samples

## [1] 1 3 7 9 11 17

Let’s estimate the genalization performance of a model using OOB samples.

iter=1000

mse.boot=rep(0,iter)

for (i in 1:iter){

set.seed(i+1)

boot.id=sample(1:20,size=20,replace=T)

f2=lm(y[boot.id]~x[boot.id])

oob.id=setdiff(1:20,boot.id)

y.hat=x[oob.id]*f2$coef[2]+f2$coef[1]

mse.boot[i]=mean((y[oob.id]-y.hat)^2)

}

mean(mse.boot)

## [1] 1.039492

hist(mse,nclass=50,xlab="MSE",ylab="Density",freq=F,main="Histogram of MSE")

abline(v=mean(f$residual^2),col="red",lwd=2)

abline(v=mean(mse),col="blue",lwd=2)

abline(v=press,col="orange",lwd=2)

abline(v=mean(mse.boot),col="brown",lwd=2)